"Should I pay my student loans first or invest in the market?"

I commonly receive this question from my colleagues, and for good reason. Nobody knows how the market will perform in the future, but you know exactly what return you will receive from paying down student loans. This question sometimes take the form of:

"What interest rate is considered high interest debt?"

In this article, I hope to provide you with the data to answer this question in a systematic manner.

Using the Historical Stock Market Performance to Evaluate the Opportunity Cost of Paying Down Debt

In a perfect situation, your threshold for paying off the loan would be an interest rate that is higher than your expected return on something you could otherwise be investing in. For most people, that would be a comparison with the stock market. Obviously, if you could predict the market, then you do not need this guide. For the rest of us, the statistical return of the stock market is a decent indicator for the long-term.

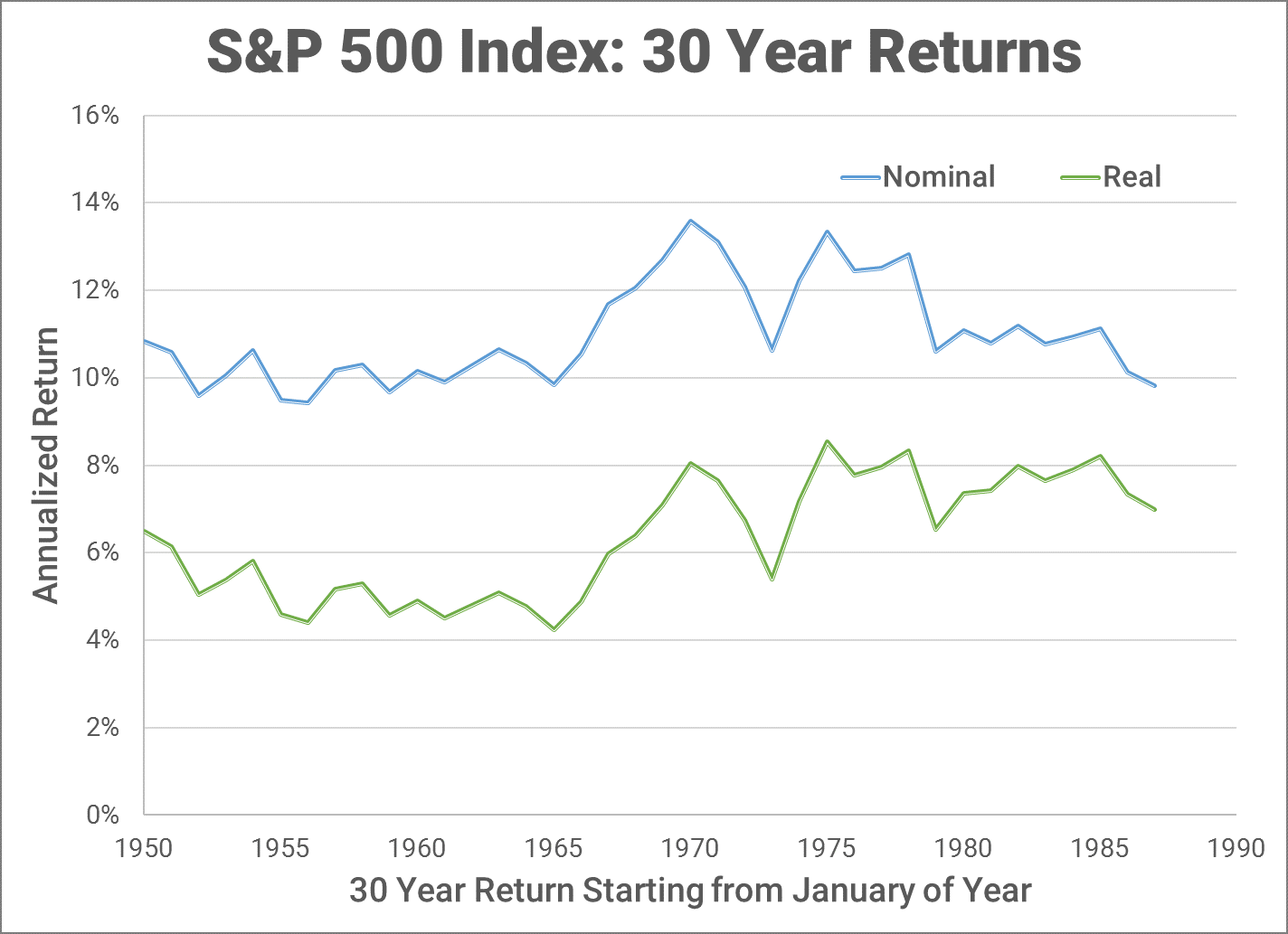

If you start investing now as a Resident or Fellow, what you invest right now in a retirement account will probably be there for at least thirty years. In a 30-year time period, the broad stock market as estimated by the S&P 500 Index has always gone up. Below is a graphical representation of the 30 year annualized return of the S&P 500 starting from a given year. For example, the return plotted in 1987 represents the 30 year time period from 1987-2017. The returns include reinvested dividends. By the way, all charts are created by me, but the values obtained from them are calculated using DQYDJ's S&P 500 Return Calculator.

Here are some defintions for you: Nominal means the pre-inflation value of, in this case, the annualized return. The Real return is the post-inflation return. Post inflation return is what we really care about.

Defining a Threshold for "High Interest Debt"

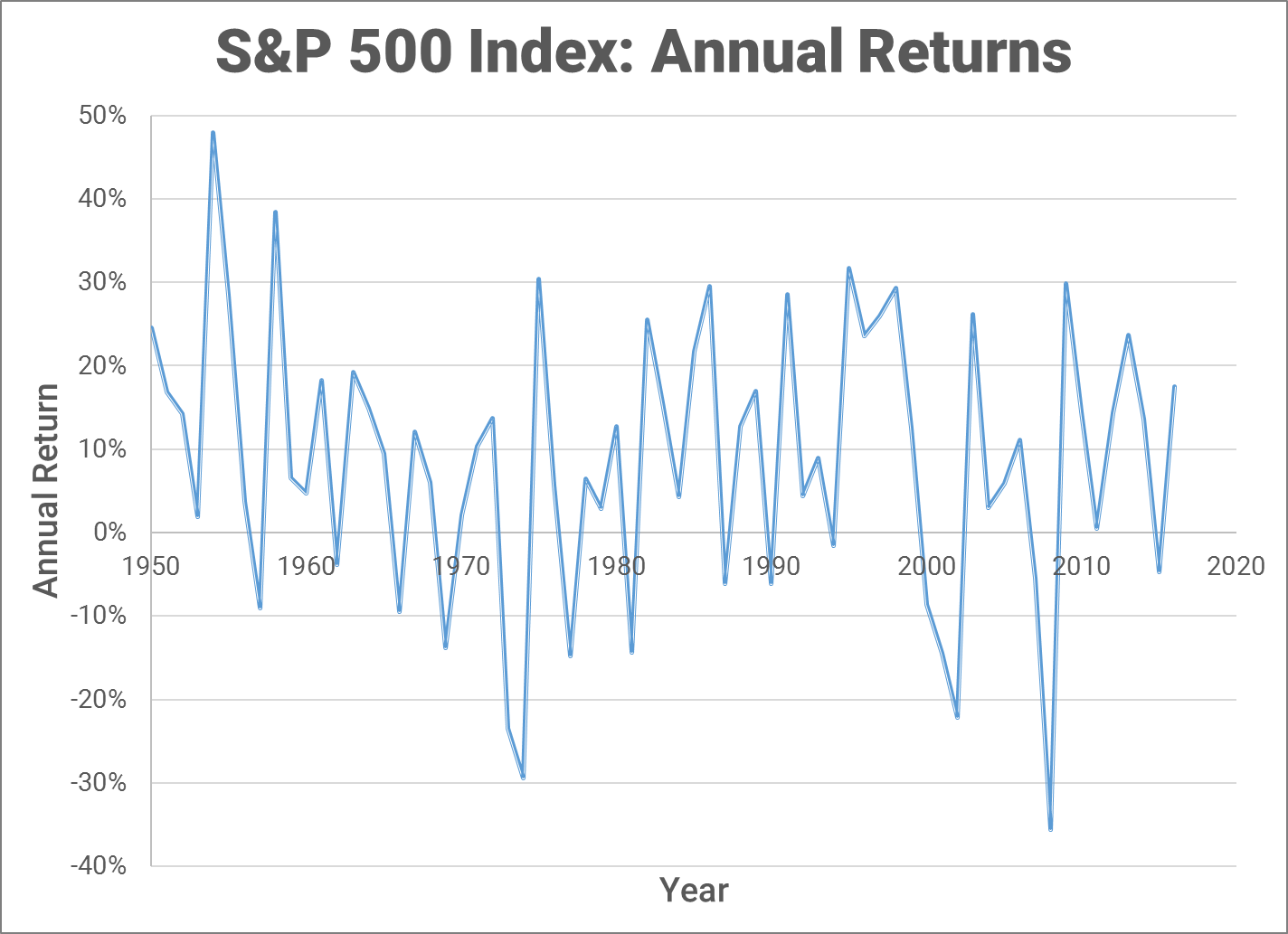

Above is a graph of the annual real return of the S&P 500 since 1950. The average real annual return of the S&P 500 since 1950 is about 8.7%, while the annualized return since 1950 is 7.3%. Either of these is a reasonable threshold to use as your personal definition of high interest debt, though personally I would choose the more conservative value. Remember that this is the REAL post-inflation return. Just as inflation reduces your investment returns, it also reduces your real interest rate. As of this writing, the average inflation rate in 2017 is 2.3%. Thus, if you were to use the 8.7% value as your cutoff, then any interest rate above 11% (8.7+2.3) could be considered high interest debt. Conversely, the cutoff for the lower value would be 9.6% (7.3+2.3).

A more conservative approach would be to evaluate some statistics of the 30 year returns and choose a percentile according to your risk tolerance. Below is a table of the percentiles (in deciles) of the 30-year returns of the stock market since 1950.

Percentile |

Annualized Return |

| 10% | 4.6% |

| 20% | 4.9% |

| 30% | 5.1% |

| 40% | 5.7% |

| 50% | 6.4% |

| 60% | 7.0% |

| 70% | 7.4% |

| 80% | 7.8% |

| 90% | 8.1% |

You can see that the volatility of the stock market is mitigated by time. Even if you consider some of the largest stock market crashes since the year 2000, a 30-year time horizon still yielded decent returns. If your 30-year time period ended right after the dot-com burst of 2001-2002, you would still have 5.4% annualized returns. Similarly, if you retired right after the housing bubble crash of 2008, your annualized returns would still have been 6.5%, and that includes the dot-com burst in its returns! That being said, you should not have a huge stock exposure when you are close to retirement age, so a crash like this occurring near your retirement age hopefully will not affect you drastically...

Choose a percentile that seems reasonable to you without overly optimistic expectations of stock market returns. For instance, you could choose the 30th percentile. This means that 70% of the time, a 30-year time period would outperform this value of 5.1%. If we were to use this as our threshold, then we would consider any interest above 7.4% (5.1+2.3) as "high interest debt".

Once you have defined what constitutes "high interest debt" for you, then you have a data-supported (or as one might call evidenced-based) threshold past which you would pay down first.

Summary

I provided several different ways to calculate a threshold to consider "high interest debt." A more optimistic approach would suggest that you pay down any loans with interest higher than 11%, and invest in the market if the interest rate is below that. A more conservative approach would set the limit at 7.4%. The true value is more nebulous, but choose based on what makes you most comfortable!